Hitting the Sweet Spot of Credit: Enhanced Income and Flexibility

Executive Summary

Global capital markets have seen increased volatility in 2023, with a combination of persistent inflation, broader fears of contagion from the banking crisis, and a recent stretch of weaker economic data are keeping investors on edge. As a result, we have experienced heightened market turmoil, increased dispersion, and wider credit spreads, even as market conditions continue to evolve. Against this backdrop, investors are therefore faced with the challenge of finding attractive, income-oriented solutions that offer a defensive source of yield, particularly as many traditional fixed income strategies (proxy: Bloomberg Global Aggregate Bond Index) have suffered from significant volatility and negative monthly returns over the last year.

To solve for this conundrum, Ares seeks to unearth investment solutions offering higher yields and diversification in what we view as more senior, higher quality segments of the corporate debt and alternative credit universes; we call it the “sweet spot” of credit. This encompasses a $5.8 trillion1 opportunity set across U.S. and European loans, corporate bonds, and alternative credit markets.

Importantly, we believe a dynamic, flexible approach to investing in the “sweet spot” of credit offers:

Against the backdrop of today’s rapidly changing and volatile market environment, we believe Ares’ global multi-asset credit strategies, including Ares Global Credit Income Fund (“AGCIF” or “the Fund”) are a potential solution for investors seeking stable, defensive sources of income. Notably, the Fund features an attractive go-forward return opportunity with a tactical asset allocation approach and disciplined fundamental credit underwriting.

A Flexible Solution for a New Rate Regime

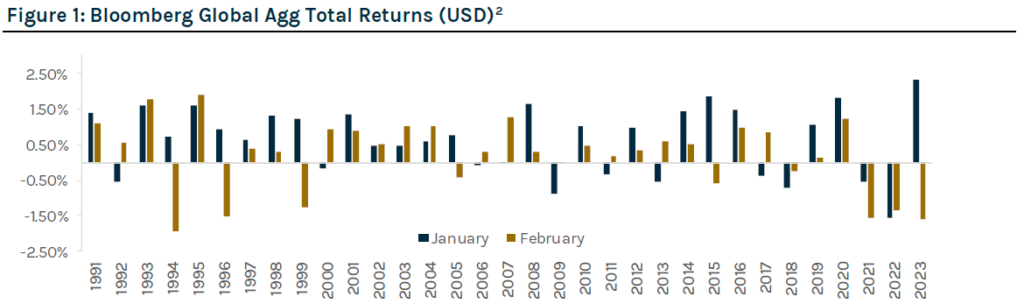

Within fixed income, traditional investment solutions, long viewed as a safe haven from equity price volatility, have not lived up to that expectation, exhibiting double digit declines in 2022 and heightened volatility year-to-date. Specifically, after a strong rally across financial markets in January of this year, February was a nasty throwback to the sort of market conditions that battered fixed income assets in 2022. As illustrated in Figure 1, the Bloomberg Global Aggregate Bond Index (the “Global Agg”) was up over 2% in January, only to decline almost 2% the following month. In today’s new rate regime, low credit risk no longer goes hand-in-hand with low mark-to-market volatility.

Global rate hiking regimes commenced in 2022 as the Federal Reserve, European Central Bank and Bank of England moved quickly to combat elevated inflation. Fast forward through today, there is more uncertainty now than ever before about the future path of monetary policy.

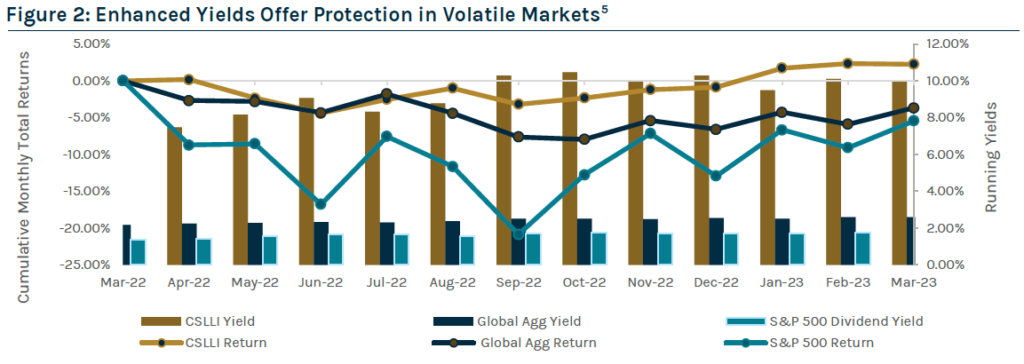

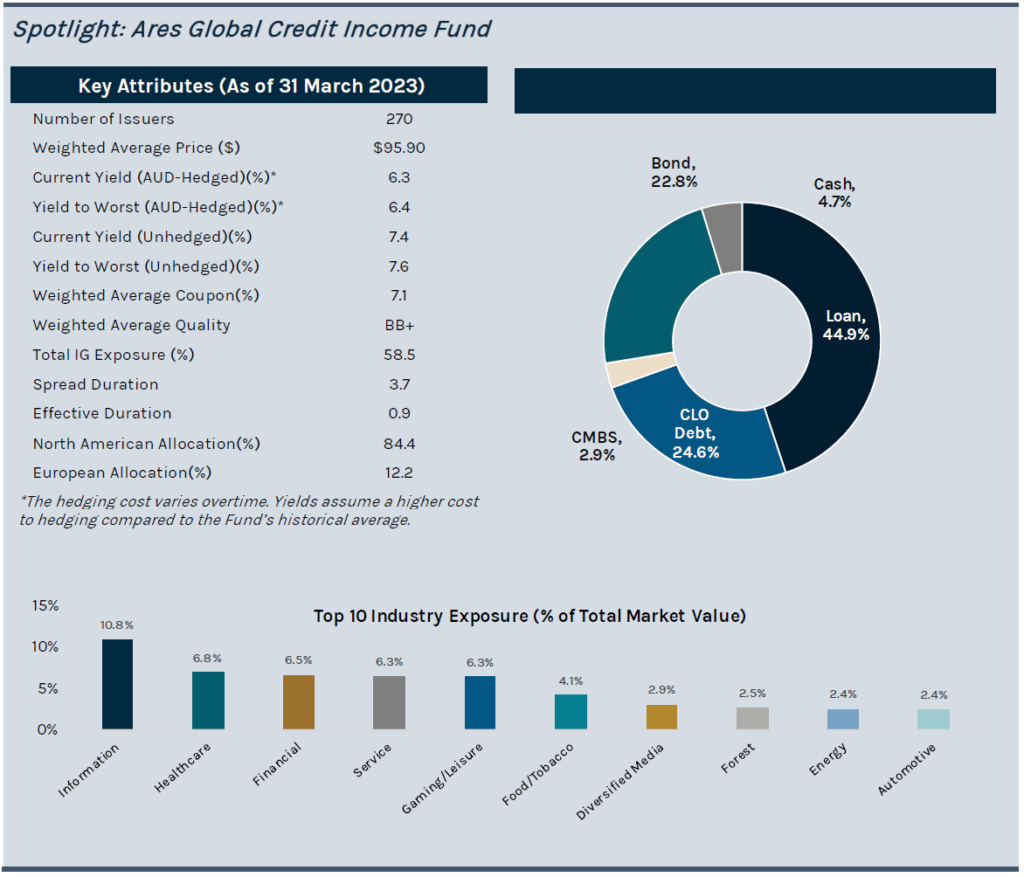

Given the expectation for continued volatility and macro uncertainty in the months ahead, we believe high income generating portfolios can help provide a buffer against choppy price movements. As illustrated in Figure 2, the Global Agg has a running yield of 2.6% with a duration of over 8 years and has declined 3.9% during the last 12-month period ending 31 March 2023, as compressed fixed rates have done little to mitigate price movements driven by elevated rate volatility. Conversely, U.S. bank loans (proxy: Credit Suisse Leveraged Loan Index) are up 2.1% for the last twelve-month period, are yielding 10.0% and have a significantly lower duration profile relative to traditional fixed income markets given the floating rate nature of the asset class. Specifically, the coupon of floating rate assets adjusts to shifts in short-term interest rates, and as a result, these assets exhibit lower price sensitivity relative to fixed rated securities. With over 70% exposure to floating rate assets today, Ares Global Credit Income Fund (“AGCIF” or the “Fund”), a liquid alternative credit portfolio, serves as a more defensive and stable source of income relative to fixed rated securities. Further, AGCIF has returned 0.5% gross (-0.4% net) for the 1-year period ending 31 March 20233, all while moving up in credit quality with approximately 58% of the portfolio allocated to investment grade credit.4

Across the preponderance of Ares’ multi-asset credit portfolios, including AGCIF, we seek to find the most attractive relative value opportunities in the “sweet spot” of credit to deliver enhanced yields with optimal downside protection and lower volatility. In today’s rapidly evolving market, we believe nimble and active portfolio management remains key to capitalizing on intermittent bouts of volatility, as they often result in attractive, but short-lived entry points.

Market Opportunity

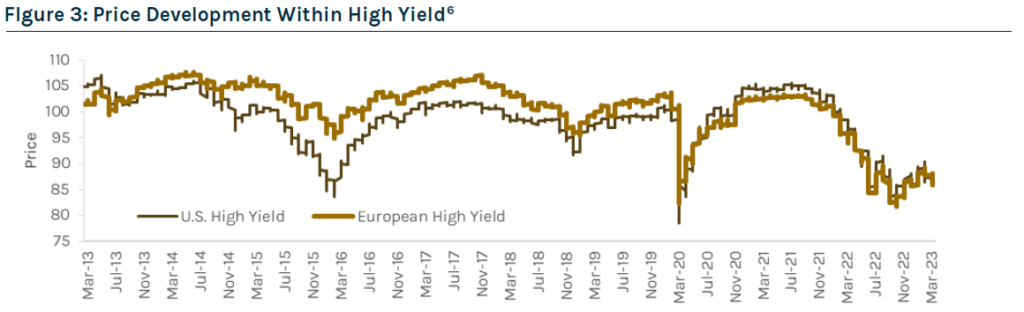

Higher yields and a decline in asset prices have introduced greater upside convexity in leveraged credit markets for total return investors, particularly for high yield bonds. As illustrated in Figure 3, today’s average price of U.S. high yield bonds is 88 cents on the dollar, presenting a compelling investment opportunity – assuming the bond does not default, a bond’s price will benefit from a natural “pull” to the nominal value as it approaches maturity, resulting in a capital gain. The proportion of the high yield market currently trading below par is approaching levels not seen since the COVID dislocation in March 2020 and the commodity crisis in 2015. With convexity in high yield bonds’ favour, we believe there is greater upside potential than downside risk as borrowing costs remain elevated.

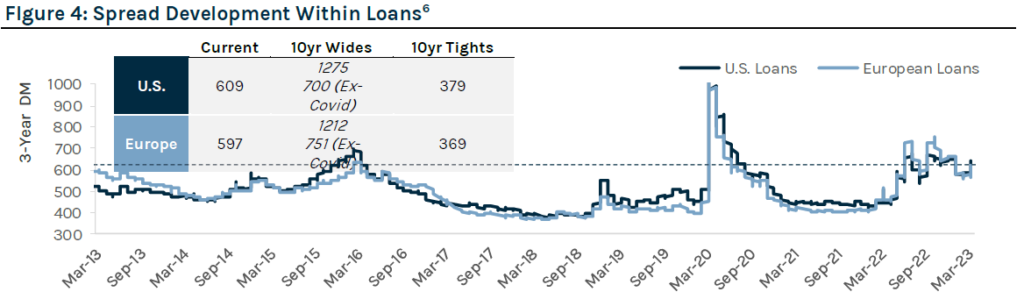

In addition to the attractive opportunity in high yield bond markets, we also believe there is a compelling case to be made for bank loans. As illustrated in Figure 4, the current average spread on loans presents an attractive opportunity as levels are greater than 70% of historical spread levels for the 3-year, 5-year, and post-Global Financial Crisis periods. Therefore, even in a recessionary environment, loan spreads have limited room to move significantly higher.

Further, loans continue to generate attractive cash yields in the high single-digits, providing a buffer to potential price volatility.

We believe this combination of higher yields, cheaper prices and wider spreads in an environment where bouts of volatility have become shorter and more frequent presents meaningful alpha-generating opportunities for active managers like Ares.

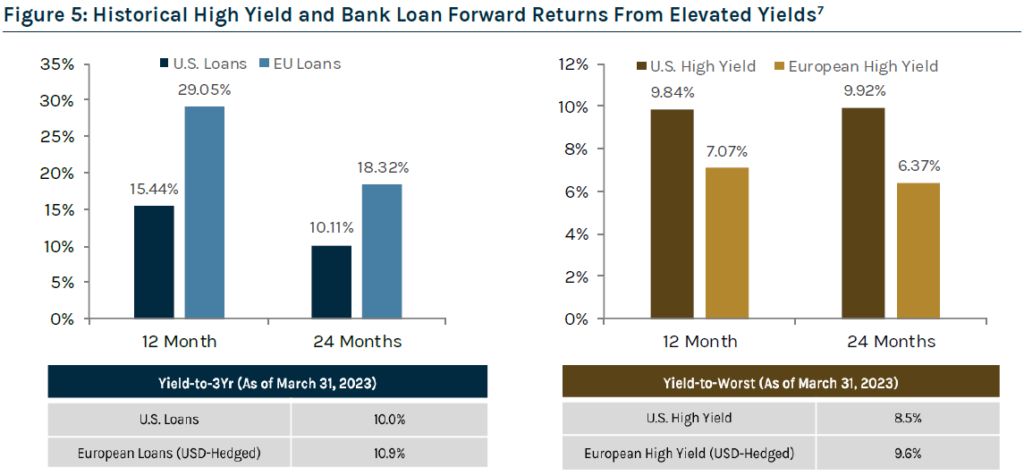

As highlighted in Figure 5, history suggests investing in periods of dislocation provides an attractive go-forward return opportunity in leveraged credit. Looking ahead, we expect attractive loan and high yield returns in the next 12-18 months given the starting point of spread, yield and discount.

Market Outlook

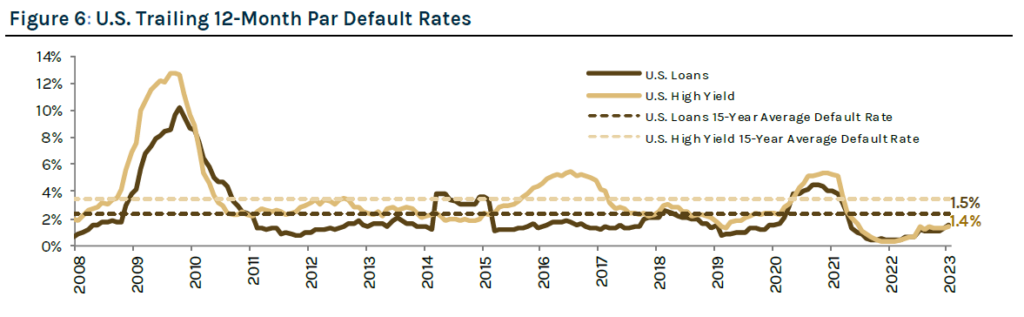

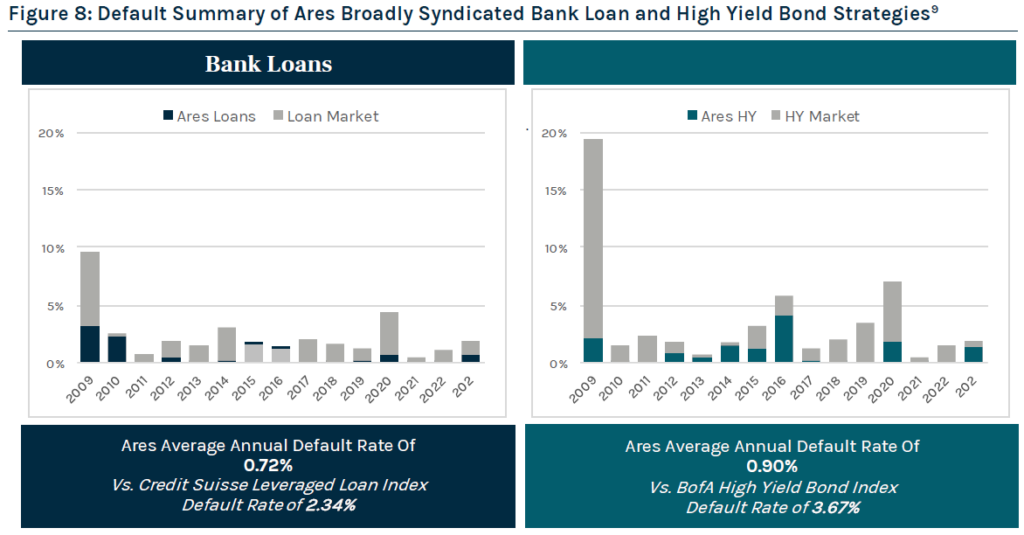

While we view the current entry point in leveraged credit to be attractive, we are closely monitoring increased tail risks. Looking forward, we anticipate that slower growth and tighter monetary policy will drive increased ratings downgrades (and defaults, to a lesser extent) and ultimately heightened volatility and dispersion. As shown in Figure 6, we have seen a modest increase in high yield bond and loan defaults in Q1’23; however, defaults remain below historical averages. In our view, there have been few unexpected defaults this year as we believe the market had already reflected the default in trading levels. In almost all cases, defaults have occurred where there is something wrong with the company’s business model rather than market stress or macro factors. And, while we anticipate defaults to rise off the lows seen in 2022, we expect them to remain manageable in the 3.5-4.5% context for 2023.

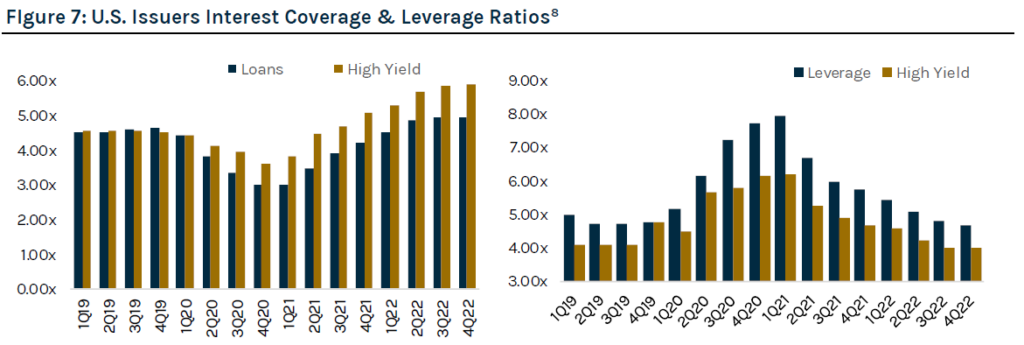

Our default outlook is further supported by stable fundamentals, as companies entered 2023 with elevated interest coverage ratios relative to history, meaning they have a greater ability to service their debt. Given many issuers refinanced at attractive levels in 2020 and 2021, most were able to push out near-term maturities and shore up liquidity to strengthen their balance sheets.

Looking ahead, we are actively monitoring downgrades, as the rating agencies have become more aggressive and proactive with 2-3 notch downgrades. That said, we believe there are certain names that are misunderstood and not deserving of the downgrade, which we view as an opportunity and will look to take advantage of post-rating action. Further, we are closely following potential downstream effects from recent events in the banking sector, including (i) a potential for contraction in financing to the tech ecosystem, (ii) negative impacts to small and medium sized businesses who are supported by regional banks, (iii) increased risks in the commercial real estate market as regional banks represent 80% of lending to this sector, and (iv) a general contraction in credit availability that further exacerbates the tightening in lending standards. Overall, we expect choppy market conditions to continue and are maintaining a steady focus on the attractive go-forward return opportunity offered in below investment grade credit.

Ultimately, we believe Ares is well positioned to employ superior credit selection and vigilant risk management in the wake of increased dispersion due to our disciplined investment process that focuses on capital preservation, predicated on bottom-up fundamental research with the goal of minimizing default risk by identifying and avoiding marginal quality credit. This core tenet of Ares’ investment philosophy has resulted in significantly lower defaults in our bank loan and high yield bond strategies, particularly in periods of dislocation.

We understand that investors are faced with persistent inflation and recession risk, and many may struggle to determine how best to position their credit exposure in an effort to maximize yield and mitigate risk. At Ares, our differentiated approach to capitalizing on the best risk-adjusted return opportunities across the investable universe is rooted in the scale and integration of our Global Liquid and Alternative Credit strategies, which allows us to fully leverage extensive research and origination capabilities, proprietary technologies and longstanding relationships.

Against the backdrop of today’s rapidly changing and volatile market environment, we believe AGCIF, a liquid alternative portfolio, is well positioned to navigate sustained periods of volatility in the months ahead while continuing to deliver enhanced yield. With an AUD-hedged yield-to-worst of 6.4%, an average price of 96 cents on the dollar, and duration of less than 1 year,10 we believe the Fund provides a compelling entry point given attractive forward return potential while fundamentals remain stable. In addition, with over 70% of the portfolio invested in senior and secured, floating rate credit today, AGCIF is significantly less sensitive to a move in rates, while providing a yield premium to traditional fixed income markets. In closing, as the era of low sovereign rates across the globe comes to an end, we believe flexible investment solutions anchored in floating rate credit, such as AGCIF, are poised to benefit from the go-forward market environment and serve as the new ballast within investor portfolios.

Past performance is not indicative of future results and no representation is made that stated results will be replicated. This article contains the opinions of Ares Australia Management and is neither an offer to sell, nor the solicitation of an offer to purchase, any security, the offer and/or sale of which can only be made by definitive offering docs. The opinions expressed herein are subject to change without notice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed. All charts, graphs and tables are shown for illustrative purposes only. This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. References to “downside protection” or similar language are not guarantees against loss of investment capital or value. Diversification does not assure profit or protect against market loss.

1 Source: CSLLI, Credit Suisse Western European Leveraged Loan Index, ICE BofA US High Yield Index, ICE BofA European Currency High Yield Constrained Index, Bank of America CMBS Research, Ares INsight database, and Intex. As of 31 March 2023.

2 As of 31 March 2023. Source: Bloomberg Global Aggregate Bond Index USD-Hedged.

3 As of 31 March 2023. Data Source: Fidante Partners. Past performance is not a reliable indicator of future performance.

4 As of 31 March 2023. Data Source: Ares. Reflects the risk-adjusted weighted average higher of rating using Moody’s, S&P, and Fitch. The Fund’s allocation is based on recent market conditions and is subject to change based on future market conditions at the time of investment and may differ materially from that set forth herein.

5 For illustrative purposes only. As of 31 March 2023. Please see endnotes for index definitions. Sources: CSLLI. S&P 500, Bloomberg Global Aggregate Bond Index USD-Hedged.

6 illustrative purposes only. As of March 31, 2023. Please see endnotes for index definitions.Sources: U.S. high yield represented by the HUC0, European high yield represented by the HPC0, U.S. Bank Loans represented by the CSLLI and European bank loans represented by the CSWELLI.

7 Note: For illustrative purposes only. Forecasts are inherently limited and should not be relied upon as indicators of actual or future outcomes. The period of analysis is from January 1997 to March 2023. Sources: HUC0, HPC0, CSLLI, CSWELLI.

8 For illustrative purposes only. Please refer to Endnotes for index definitions. Source: JPM, 4Q22 Loan and High Yield Credit Fundamentals Report.

9 LTM annual average par-weighted default rates for the period January 1, 2009 – March 31, 2023. U.S. bank loan default rates represented by the CSLLI. Ares bank loan default rates are represented by all bank loan transactions in all commingled funds and separately managed accounts executed by investment professionals within Ares Liquid Credit Group. U.S. high yield default rates are represented by the H0A0. Ares high yield default rates are represented by all high yield bond transactions in all commingled funds and separately managed accounts executed by investment professionals within Ares Liquid Credit Group.

10 As of 31 March 2023.

Index Disclosure & Definitions

Index Disclosure: Indices are provided for illustrative purposes only and not indicative of any investment. They have not been selected to represent appropriate benchmarks or targets for the strategy. Rather, the indices shown are provided solely to illustrate the performance of well-known and widely recognized indices. Any comparisons herein of the investment performance of a strategy to an index are qualified as follows: (i) the volatility of such index will likely be materially different from that of the strategy; (ii) such index will, in many cases, employ different investment guidelines and criteria than the strategy and, therefore, holdings in such strategy will differ significantly from holdings of the securities that comprise such index and such strategy may invest in different asset classes altogether from the illustrative index, which may materially impact the performance of the strategy relative to the index; and (iii) the performance of such index is disclosed solely to allow for comparison on the referenced strategy’s performance to that of a well-known index. Comparisons to indices have limitations because indices have risk profiles, volatility, asset composition and other material characteristics that will differ from the strategy. The indices do not reflect the deduction of fees or expenses. You cannot invest directly in an index. No representation is being made as to the risk profile of any benchmark or index relative to the risk profile of the strategy presented herein. There can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable, equal any corresponding indicated historical performance or be suitable for a portfolio. The information related to the various indices is sourced from the providers’ websites. Ares is not responsible for any historic revision made to the indices.

The Bloomberg Barclays Capital Global Aggregate Bond Index (“Barclays Global Agg”) measures the performance of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging market issuers. To be included in the index, bonds must be investment grade using the index credit quality classification methodology (middle rating of Moody’s, Fitch and S&P). The currency must be freely tradeable and convertible and not exposed to exchange controls that are designed to encumber its buying and selling by foreign investors. There must be an established and developed forward market or non-deliverable forward (NDF) market for the local currency such that foreign market participants can hedge their exposures into core currencies. Inception date: January 1, 1990.

The Credit Suisse Western European Leveraged Loan Index (“CSWELLI”) is designed to mirror the investable universe of the leveraged loan market of issues which are denominated in US$ or Western European currencies. The issuer has assets located in or revenues derived from Western Europe, or the loan represents assets in Western Europe, such as a loan denominated in a Western European currency. Loan facilities must be rated “5B” or lower. That is, the highest Moody’s/S&P ratings are Baa1/BB+ or Ba1/BBB+. Only fully funded term loan facilities are included and the tenor must be at least one year. Minimum outstanding balance is $100 million and new loans must be priced by a third-party vendor at month-end. The index inception is January 1998.

The Credit Suisse Institutional Leveraged Loan Index (“CSLLI”) is designed to mirror the investable universe of the $US-denominated leveraged loan market. The index inception is January 1992. The index is priced daily and rebalanced monthly. New loans are added to the index on their effective date if they qualify according to the following criteria: 1) Loan facilities must be rated “5B” or lower. That is, the highest Moody’s/S&P ratings are Baa1/BB+ or Ba1/BBB+. If unrated, the initial spread level must be Libor plus 125 basis points or higher. 2) Only fully-funded term loan facilities are included. 3) The tenor must be at least one year. 4) Issuers must be domiciled in developed countries; issuers from developing countries are excluded.

ICE BofA European Currency High Yield Index (“HPC0”) tracks the performance of EUR and GBP denominated below investment grade corporate debt publicly issued in the eurobond, sterling domestic or euro domestic markets. Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Fitch) and an investment grade rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long term sovereign debt ratings). In addition, qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of EUR 100 million or GBP 50 million. Original issue zero coupon bonds, “global” securities (debt issued simultaneously in the eurobond and domestic markets), 144a securities and pay-in-kind securities, including toggle notes, qualify for inclusion in the Index. Callable perpetual securities qualify provided they are at least one year from the first call date. Fixed-to-floating rate securities also qualify provided they are callable within the fixed rate period and are at least one year from the last call prior to the date the bond transitions from a fixed to a floating rate security. Defaulted, warrant-bearing and euro legacy currency securities are excluded from the Index. Inception date: December 31, 1997 The above rules take into account all revisions up to and including December 31, 2010.

The BofA US High Yield Master II Constrained Index (“HUC0”) tracks the performance of US Dollar denominated below investment grade corporate debt publicly issued in the US domestic market with a maximum issuer exposure of 2%. The index is priced daily and rebalanced monthly. The returns of the benchmark are provided to represent the investment environment existing during the time period shown. For comparison purposes the index includes the reinvestment of income and other earnings but does not include any transaction costs, management fees or other costs. ICE BANK OF AMERICA IS LICENSING THE ICE BofA INDICES AND RELATED DATA “AS IS,” MAKES NO WARRANTIES REGARDING SAME, DOES NOT GUARANTEE THE SUITABILITY, QUALITY, ACCURACY, TIMELINESS, AND/OR COMPLETENESS OF THE ICE BofA INDICES OR ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM, ASSUMES NO LIABILITY IN CONNECTION WITH THEIR USE, AND DOES NOT SPONSOR, ENDORSE, OR RECOMMEND ARES MANAGEMENT, OR ANY OF ITS PRODUCTS OR SERVICES.

The S&P 500 is an American stock market index based on the market capitalisations of 500 large companies having common stock listed on the NYSE or NASDAQ. The S&P 500 index components and their weightings are determined by S&P Dow Jones Indices

Disclaimer

This material has been prepared by Ares Australia Management Pty Ltd ABN 51 636 490 732 AFSL 537666 (AAM), the investment manager of the Ares Global Credit Income Fund (ARSN 639 123 112) (the Fund) and is current as at the date of publication. Fidante Partners Limited ABN 94 002 835 592 AFSL 234668 (Fidante) is a member of the Challenger Limited group of companies (Challenger Group) and the responsible entity of the Fund. Other than information which is sourced from Fidante in relation to the Fund, Fidante is not responsible for the information in this publication, including any statements of opinion. It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. You should consider, with a financial adviser, whether the information is suitable to your circumstances. The Fund’s Target Market Determination and Product Disclosure Statement (PDS) available at www.fidante.com should be considered before making a decision about whether to buy or hold units in the Fund(s). To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.

Past performance is not indicative of future performance. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Fidante has entered into arrangements with Ares and AAM in connection with the distribution and administration of financial products managed by Ares or AAM. In connection with those arrangements, Fidante or AAM may receive remuneration or other benefits. Fidante is not an authorised deposit-taking institution (ADI) for the purpose of the Banking Act 1959 (Cth), and its obligations do not represent deposits or liabilities of an ADI in the Challenger Group (Challenger ADI) and no Challenger ADI provides a guarantee or otherwise provides assurance in respect of the obligations of Fidante. Investments in the Fund are subject to investment risk, including possible delays in repayment and loss of income or principal invested. The performance, the repayment of capital or any particular rate of return on your investments are not guaranteed by any member of the Challenger Group nor AAM or its related bodies corporate.

No reliance: This publication is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The publication has not been independently verified. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees, make any republications, warranty or undertaking (express or implied) and accepts no responsibility for the adequacy, accuracy, completeness or reasonableness of the publication or as to the performance of any product. The information contained in the publication does not purport to be complete and is subject to change. No reliance may be placed for any purpose on the publication or its accuracy, fairness, correctness or completeness. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the publication or otherwise in connection with the publication. Any forward-looking statements in this publication: are made as of the date of such statements; are not guarantees of future performance; and are subject to numerous assumptions, risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Ares undertakes no obligation to update such statements. Past performance is not a reliable indicator of future performance.

Confidentiality and intellectual property: This publication is confidential and may not be copied, reproduced or redistributed, directly or indirectly, in whole or in part, to any other person in any manner.

Risk: no person guarantees the performance of, or rate of return from, any product or strategy relating to this publication, nor the repayment of capital in relation to an investment in such product or strategy. An investment in any such product or strategy is not a deposit with, nor another liability of, Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd nor any of their respective related bodies corporates, associates or employees. Investment in any product or strategy relating to this publication is subject to investment risks, including possible delays in repayment and loss of income and capital invested.

REF: AAM-00381